Newsmax’s Stock Plunge Sheds Light on Seeking Alpha’s Policies — and Raises Bigger Questions

By Rick LaRivière

A Fast Response or a Cover-up?

On May 23, 2025, several journalists asked Seeking Alpha CEO David Jackson tough questions: How does your platform stop anonymous short sellers from using your site to tank stocks and profit?

One inquiring journalist, John Tabacco, has been a guest contributor to this outlet and is also an on-air media personality on Newsmax (NMAX).

The information sought was simple: explain how Seeking Alpha verifies the real identities and financial affiliations of anonymous contributors when publishing bearish articles, particularly recently about Newsmax stock.

Four days later, on May 27, 2025, Jackson’s team responded, saying they “see no evidence” of manipulation in Newsmax’s “collapse” and pointing to the Seeking Alpha website for answers.

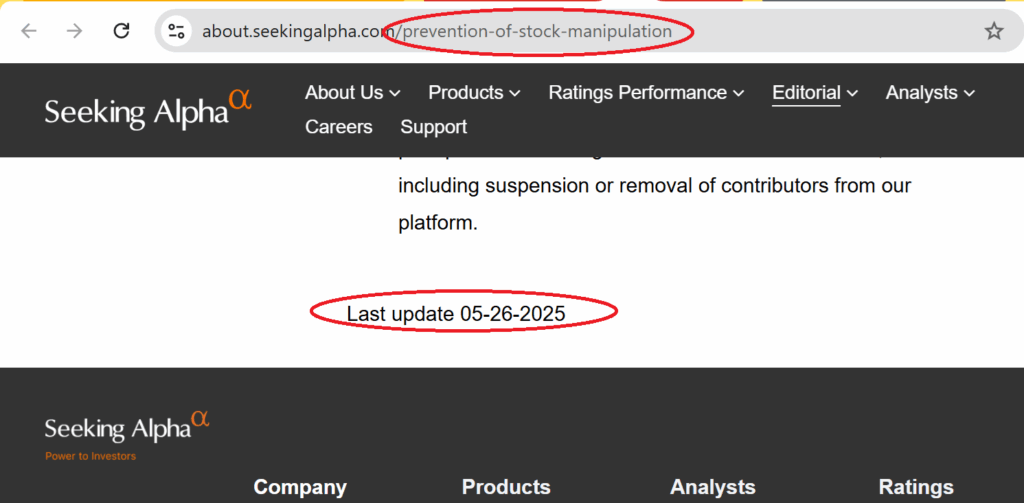

But here’s the catch: that same website was updated on Memorial Day, May 26, 2025.

While most Americans were flipping burgers or knocking back drinks, Seeking Alpha’s compliance team was hard at work updating their “Prevention of Stock Manipulation” policy.

Is that diligence — or a desperate scramble to cover their tracks?

Jackson’s reply email (reproduced in full below) says Seeking Alpha “authenticates real names of pseudonymous contributors” and “enthusiastically cooperates with the SEC.”

But the response reads alarmingly like lawyer-approved, AI-generated babble. There were no real “answers,” just window dressing.

The big question still hangs in the air: Does Seeking Alpha verify the real identities and financial affiliations of anonymous contributors?

If not, how can they claim to prevent the very market manipulation outlawed by SEC Rule 10b-5?

The Newsmax Case: A Familiar Pattern?

Newsmax’s IPO story reads like a case study in manipulation. Its stock surged from $10 to $233 in days — then crashed to the low $20s.

Critics say Seeking Alpha’s flood of negative articles fueled the panic, echoing a classic “short and distort” campaign.

Seeking Alpha denies this.

“Newsmax’s stock history suggests the spike was itself the aberration,” Jackson wrote. He says bearish articles by real investors warned about Newsmax’s “operating losses, negative cash flow, legal risks, and dependence on advertising.” He insists there was no rumor-mongering — just sound analysis.

But Professor Joshua Mitts of Columbia Law School has seen this play before.

In his 2018 study, Mitts found that pseudonymous Seeking Alpha posts were often preceded by suspicious options trading. He called this tactic “short and distort” — a ploy to profit by driving prices down with online posts and secret bets.

“This is not about short selling itself,” Mitts said. “It’s about potential abuse and securities fraud.”

His work has already fueled a Justice Department probe into activist short sellers and their online allies. As Mitts puts it, “My goal is to understand how these short reports impact markets.”

Unbelievable Compliance or Manipulation: A Platform Built for Profit — But for Whom?

Seeking Alpha says it doesn’t take payments from hedge funds, investment firms, or companies to publish articles.

“Our model aligns with subscribers, not stock manipulators,” Jackson says.

The platform claims it doesn’t hold stock positions or make money on price swings.

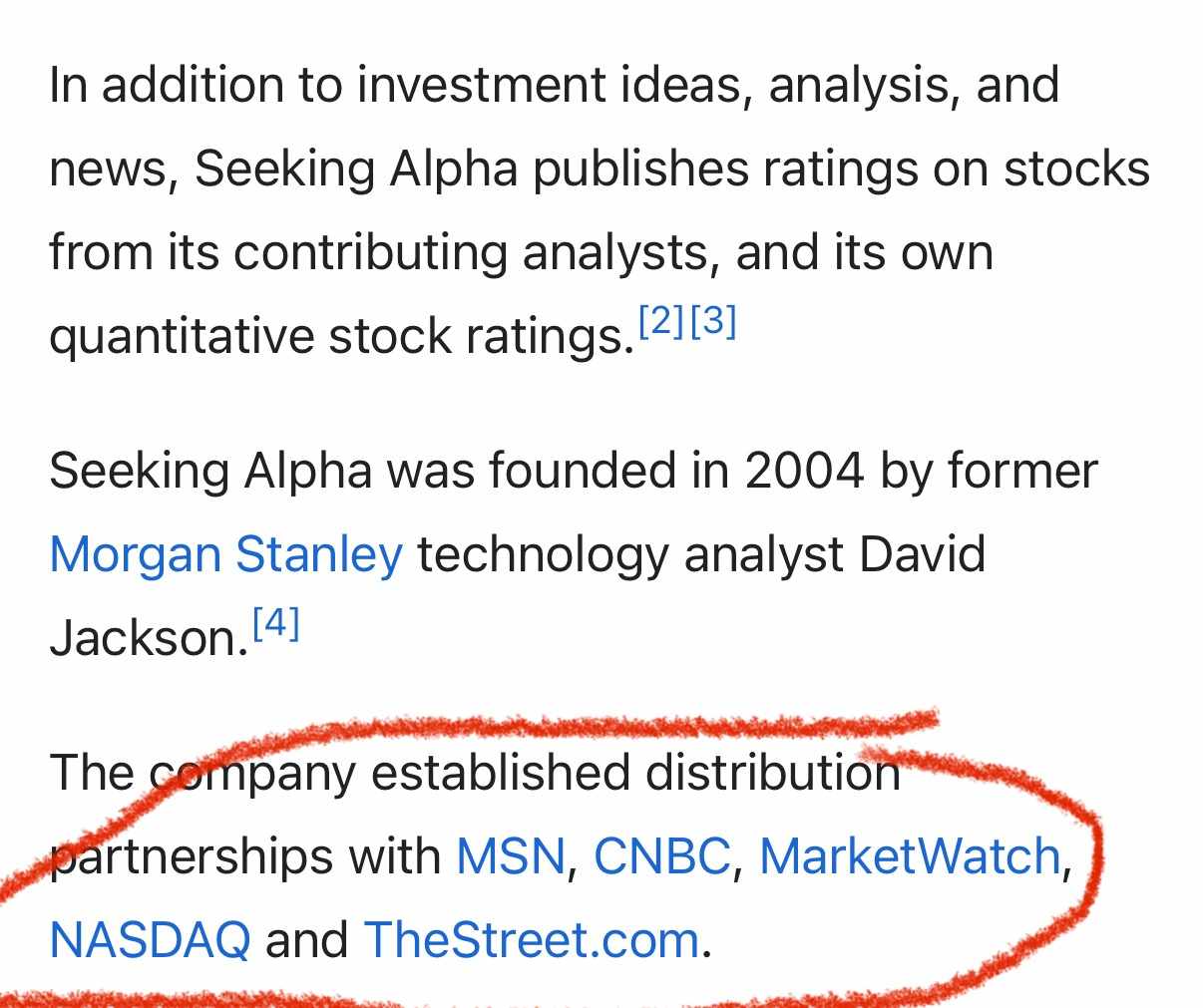

Yet, Seeking Alpha’s strategic partnerships with MSN, CNBC, MarketWatch, NASDAQ, and TheStreet.com raise red flags. The company’s Wikipedia page prominently displays these connections.

These sites syndicate Seeking Alpha’s articles, boosting the reach of every bearish hit piece.

Critics ask: How objective can Seeking Alpha really be if it’s embedded in these big media machines?

The bigger problem is Seeking Alpha’s policy on pseudonymous contributors. Although they say they “verify” real names and contact information, they keep it secret.

Verification alone doesn’t stop manipulation. As Mitts and others argue, the real risk is that shadow contributors can hide conflicts of interest while moving markets.

Unbelievable Compliance or Manipulation: Old Habits Die Hard

Seeking Alpha’s history with market chaos runs deep. From MiMedx to Aphria to CytRx, the pattern is the same: sudden negative articles, plunging stock prices, and lawsuits or investigations to follow.

In each case, Seeking Alpha insists it was just hosting legitimate research.

Jackson says the platform has improved oversight since Mitts’ 2018 report, which slammed Seeking Alpha for enabling identity switching. New rules limit contributors to a single pseudonym.

Still, critics argue the core problem remains: a system built to publish thousands of opinions, without enough guardrails to weed out the bad actors.

On May 23, 2025, we asked Seeking Alpha a series of detailed questions to put the issue to bed:

From: Rick LaRivière <RickLaRiviere@proton.me>

Date: On Friday, May 23rd, 2025 at 6:14 AM

Subject: Formal Media Inquiry Regarding Contributor Accountability, Market Manipulation, and Coverage of Newsmax (NMAX)

To: joelh@seekingalpha.com <joelh@seekingalpha.com>, privacy@seekingalpha.com <privacy@seekingalpha.com>, subscriptions@seekingalpha.com <subscriptions@seekingalpha.com>, analysts@seekingalpha.com <analysts@seekingalpha.com>, marketplace@seekingalpha.com <marketplace@seekingalpha.com>

CC: RALafontaine@protonmail.com <ralafontaine@protonmail.com>, richard.luthmann@protonmail.com <richard.luthmann@protonmail.com>, frankiepressman@protonmail.com <frankiepressman@protonmail.com>, mthomasnast@protonmail.com <mthomasnast@protonmail.com>, mvolpe998@gmail.com <mvolpe998@gmail.com>Dear Mr. Hancock and Seeking Alpha Leadership,

We are independent journalists currently investigating a series of reports concerning potential misuse of the Seeking Alpha platform to influence financial markets, particularly through pseudonymous short seller campaigns.

Our investigation involves specific allegations and documented cases of irregular market activity. Seeking Alpha content appears to have played a central role in amplifying price volatility, notably in the case of Newsmax (NMAX) following its IPO.

We are preparing a report for publication and would appreciate your response to the following questions to ensure the accuracy and fairness of our coverage.PLATFORM STRUCTURE AND ACCOUNTABILITY

1. Does Seeking Alpha verify the real identities and financial affiliations of anonymous or pseudonymous contributors? If not, how does the platform prevent potential violations of SEC Rule 10b-5?

2. What safeguards are in place to prevent authors from publishing articles while holding undisclosed positions—particularly short positions—in the securities they write about?

3. Can Seeking Alpha provide statistics on the number of current contributors who are anonymous, the number who have disclosed financial positions, and the number who have been disciplined or removed for misconduct?

4. Why does Seeking Alpha allow ghostwritten or team-authored articles under single pseudonyms, and how does that align with your claim to provide transparent investment research?

5. Is there a formal review process for identifying patterns of coordinated article publication (e.g., same stock, similar thesis, short timeframe) which may indicate a “short-and-distort” campaign?MARKET IMPACT AND MANIPULATION CLAIMS

6. Is Seeking Alpha aware of cases where its articles have been linked to rapid stock declines or subsequent shareholder litigation (e.g., MiMedx, Aphria, BioZoom, CytRx)? How did the company respond?

7. How does the platform distinguish between legitimate bearish analysis and potentially manipulative content intended to trigger panic selling?

8. Has Seeking Alpha ever investigated whether contributors or entities may be using the platform as a coordinated tool to front-run trades or distort public markets? If so, what were the findings?

9. What responsibility does Seeking Alpha take when a published article contributes to a measurable stock price drop, especially in thinly traded or microcap stocks?

10. Is there any auditing mechanism that tracks whether contributors publish shortly before or after taking financial positions in a stock?ALGORITHMIC AMPLIFICATION AND DISTRIBUTION

11. Does Seeking Alpha monitor the downstream effects of its content once syndicated to platforms like Bloomberg Terminal, Yahoo Finance, and Google News?

12. Are algorithmic signals and news aggregators considered in the editorial process, given that a single article may trigger institutional-level sell-offs or high-frequency trading?

13. What editorial standards or disclosures are required for articles covering illiquid stocks that may be especially vulnerable to manipulation once distributed to algorithmic platforms?PATTERNS AND REPEAT OFFENDERS

14. Has Seeking Alpha identified repeat contributor accounts that routinely publish bearish content leading to stock price declines? What measures are taken when such patterns emerge?

15. Does the platform track cross-posting amplification strategies (e.g., contributors’ use of Reddit, Twitter, and StockTwits to artificially magnify reach and impact)?

16. How does Seeking Alpha prevent third parties—hedge funds, activist short sellers, or foreign entities—from covertly sponsoring contributors to advance narratives?FINANCIAL INCENTIVES AND OUTSIDE FUNDING

17. Are contributors financially incentivized based on traffic, views, or stock movement, thereby encouraging sensationalized or market-moving content?

18. Has Seeking Alpha received any financial support, advertising revenue, or partnership funding from short-focused hedge funds, research firms, or related interest groups?

19. Is Seeking Alpha aware of any third-party ghostwriting arrangements or pay-for-publication schemes involving its contributors and institutional short sellers?

20. Was any editorial or promotional support for coverage of Newsmax (NMAX) or other meme-era stocks linked to known short-interest parties or hedge funds?THE NEWSMAX (NMAX) CASE

21. Did Seeking Alpha’s editorial staff review the timing and tone of bearish articles on Newsmax relative to its IPO and initial surge?

22. Were any contributors who wrote negatively about Newsmax (NMAX) holding short positions or working on behalf of entities that were short? Were those conflicts disclosed?

23. Does Seeking Alpha recognize that multiple bearish pieces on Newsmax appeared within days of its IPO, echoing language from past short campaigns (e.g., “overvalued,” “meme stock,” “unsustainable”)?

24. Given Newsmax’s stock collapse from a $30B valuation to below $10B within days, does Seeking Alpha consider its own editorial coverage to have contributed to or amplified the decline?

25. Will Seeking Alpha publish a full transparency report or internal audit regarding its role in the NMAX decline and disclose any relationships between contributors and short-positioned entities?REGULATORY AND LEGAL POSITION

26. Has Seeking Alpha ever been contacted by the SEC, FINRA, or DOJ regarding market manipulation or the publication of misleading or conflict-ridden articles?

27. If subpoenaed, does Seeking Alpha maintain contributor IP logs, payment records, and communications that would allow investigators to determine real identities and financial backers?

28. Does Seeking Alpha view itself as a publisher with editorial responsibility, or merely a platform with limited liability under Section 230?

29. Has the platform ever submitted internal misconduct, manipulation flags, or suspicious contributor behavior to federal regulators voluntarily?

30. Does Seeking Alpha believe its current structure complies with SEC Rule 10b-5, FINRA 2210, and Regulation FD? If so, what specific compliance protocols back that up?We plan on going to press soon and would like to give our readers a fair and balanced view of the facts and issues presented. If we hear from you after press time, we will be sure to incorporate your responses in a follow-up.

Again, we appreciate your time.

Thanks,

Rick LaRivière

Independent Journalist

On May 27, 2025, the day after their website’s Memorial Day edits, Seeking Alpha CEO David Jackson said:

From: David Jackson <david@seekingalpha.com>

Date: On Tuesday, May 27th, 2025 at 10:44 AM

Subject: Re: Formal Media Inquiry Regarding Contributor Accountability, Market Manipulation, and Coverage of Newsmax (NMAX)

To: RickLaRiviere@proton.me <RickLaRiviere@proton.me>

CC: jt@liquidlunchtv.com <jt@liquidlunchtv.com>Dear Mr Tabacco and Mr LaRiviere,

Thank you for your emails about Seeking Alpha’s coverage of Newsmax.

For information about our compliance and editorial processes, please see How Seeking Alpha Prevents its Platform From Being Used for Stock Manipulation.

Regarding Newsmax in particular:

I see no evidence of downward manipulation of Newsmax’ stock price from its trading history.

Stock manipulators try to cause changes in a stock’s price for their own profit, and their ability to manipulate stock prices is temporary. Immediately after its IPO, NMAX spiked to $83 on March 31st, and reached a peak of $233 on April 1st. From there, it fell steadily: to $52 on April 2nd, $62 on April 3rd, $45 on April 4th, $39 on April 8th, and $25.40 on April 10th. Since April 11th, Newsmax’ stock has been trading in the low or mid 20s, with no temporary spikes in the price. In other words, the decline in NMAX from its $233 peak to $20-$25 was not temporary. It’s highly unlikely that anyone trying to manipulate the stock could engineer a sustained decline followed by trading in a range in the low to mid 20s for such a sustained period of time if the un-manipulated, market clearing stock price was significantly higher. In fact, NMAX’s price history suggests that the post IPO spike to higher than the low to mid 20s was itself the market aberration, and did not reflect price discovery in a smoothly functioning market.Seeking Alpha’s coverage of Newsmax had none of the characteristics of stock manipulation.

Stock manipulators disseminate rumors or inaccurate or misleading information to influence stock prices. In contrast, the Seeking Alpha contributors who wrote bearish articles on NMAX expressed concerns about Newsmax’ operating losses, negative cash flow, legal risks, and dependence on advertising. More than anything else, they expressed concern about the stock’s valuation. All their concerns were about information provided by Newsmax in its SEC filings, or about Newsmax’ valuation. None of their concerns involved rumors or inaccurate or misleading information.

Newsmax is a spectacular example of the value Seeking Alpha brings to investors.

Many individual investors are drawn to newly public stocks post-IPO, particularly of companies whose products they use. But there’s a heightened risk that individual investors can get badly burned in these cases. There’s often a shortage of tradable shares immediately after an IPO, and when that is combined with short term demand from price-insensitive, individual investors, it can lead to the stock spiking. If individual investors buy at the spiked price, their percentage losses as the stock settles to a sustainable price can be massive. That is arguably exactly what happened with Newsmax.

Who is able to warn and protect investors in these cases? Not the investment banks which sponsored the IPO, because they are barred from issuing research on a stock in the immediate aftermath of its IPO. Even if they were able to publish research, it’s statistically improbable that an investment bank will slap a “Sell” rating on the stock of a company it took public. Other investment banks rarely issue research for newly public stocks whose IPOs they did not participate in. As a result, there was no Wall Street research covering Newsmax immediately after its IPO.

In this situation, Seeking Alpha brought tremendous value to investors. Our articles are by real investors, not analysts working for investment banks which profit from IPOs. So Seeking Alpha contributors were able to cover NMAX in the immediate aftermath of its IPO. Seeking Alpha contributors Seeking Profits, Bill Maurer, Daniel Jones and Mike Fay warned investors about Newsmax’ valuation on April 1st and April 2nd. Investors who heeded their warnings not to buy the stock on those days saved themselves a loss of about 90%.

Newsmax is one of many cases where Seeking Alpha helps investors. Seeking Alpha’s platform surfaces diverse, independent investing ideas. We embrace ideas and analysis by real investors, because they are more actionable, result in broader coverage, and perform better.Best Regards,

David Jackson,

Founder and CEO, Seeking Alpha

Unbelievable Compliance or Manipulation: The SEC’s Blind Spot

SEC Rule 10b-5 says it’s illegal to use manipulative or deceptive devices to influence a security’s price.

But free speech protections—and Seeking Alpha’s status as a media platform—make enforcement tricky. The SEC and DOJ have launched broad investigations into short sellers and their allies, but real accountability has been slow.

Meanwhile, Seeking Alpha’s “independent” contributors — who aren’t licensed investment professionals — keep publishing.

Their work can move stocks within minutes, with no accountability for financial ties or hidden motives.

Unbelievable Compliance or Manipulation: Diligence or Deception?

Jackson says Seeking Alpha’s last update to its policies was on Memorial Day. Was that a sign of remarkable diligence — or a scramble to fix exposure after journalists started asking questions?

Only Seeking Alpha knows for sure.

One thing is clear: while Seeking Alpha claims it’s the voice of independent investors, it’s also become a powerful tool for shadow campaigns.

Until regulators close the gap — or Seeking Alpha pulls back the curtain on its real editorial processes — the question of who’s really behind those pseudonymous posts will linger.

For retail investors, the lesson is simple: Caveat emptor. In the age of anonymous analysis, not every investing idea is what it seems.

Leave a Reply